Houston continues to be one of the most dynamic real estate markets in Texas. While the median home price might look attractive compared to other major coastal cities, many first-time buyers and seasoned investors alike get caught off guard at the closing table. Beyond the down payment, you must be financially prepared for closing costs.

Whether you are buying a historic bungalow in the Loop or investing in a new build in the suburbs, this guide breaks down exactly what you can expect to pay in Houston for 2026.

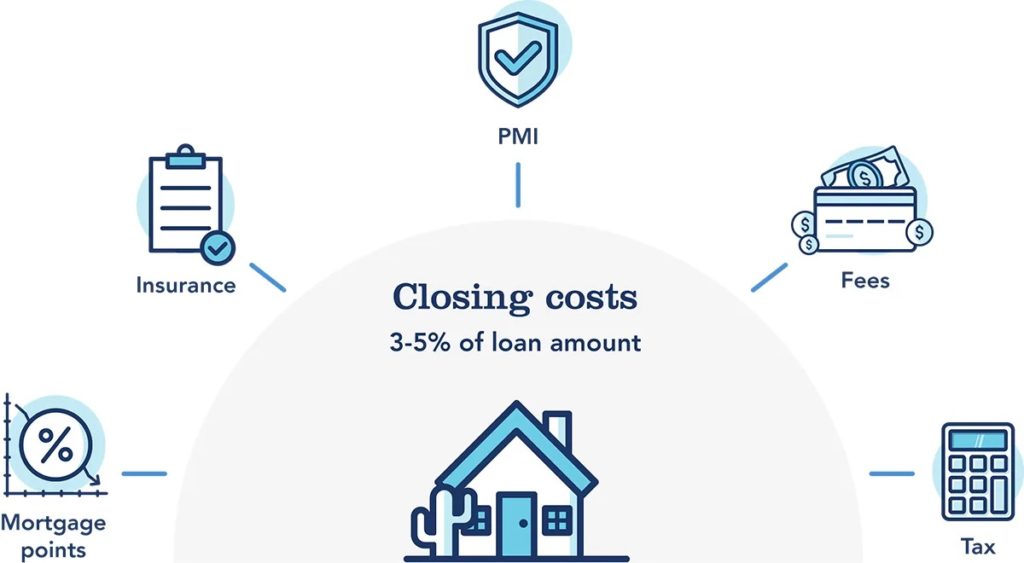

What Are Closing Costs and How Much Are They in Houston?

Closing costs are the assortment of fees, taxes, and administrative charges paid to your lender, the title company, and local government agencies to finalize a real estate transaction.

As a general rule of thumb in the Houston market:

- Buyers typically pay between 2% and 5% of the home’s purchase price.

- Sellers generally pay between 6% and 9%, with the vast majority of this going toward real estate agent commissions.

The Texas Advantage: One major financial relief for both buyers and sellers in Houston is that Texas does not charge a state or local real estate transfer tax. This can save you thousands of dollars compared to buying property in states like New York or Florida.

Buyer Closing Costs in Houston: A Complete Breakdown

When you receive your Loan Estimate, the costs will be categorized. Here is what a Houston buyer is actually paying for:

- Lender Fees: These are the costs to process your mortgage. They typically include an origination fee (often 0.5% to 1% of the loan amount), underwriting fees, and credit report charges.

- Property-Related Fees:

- Appraisal Fee ($400 – $800): Your lender requires an independent valuation of the home.

- Survey ($400 – $800): Unless the seller has an existing, valid survey and a notarized T-47 affidavit, a new boundary survey is almost always required in Texas.

- Inspections ($300 – $700+): While optional, a comprehensive physical inspection is highly recommended to uncover hidden issues.

- Title & Escrow Charges:

- Lender’s Title Insurance: A policy that protects the mortgage company against title defects. The rates are strictly regulated by the Texas Department of Insurance (TDI).

- Escrow and Prepaids: This is often the largest chunk of a buyer’s cash to close. Lenders typically require you to prepay a portion of your annual property taxes (usually 3 to 4 months) and your first year of homeowners insurance (plus a 2-month cushion) into an escrow account.

Hidden Closing Costs Unique to the Houston Market

Standard national calculators often underestimate Houston closing costs because they miss the nuances of the local market. Here is what you need to watch out for in 2026:

- High Property Taxes & MUD Taxes: Texas has no state income tax, which means local municipalities rely heavily on property taxes. When estimating your escrow prepaids, particularly for new urban developments in rapidly expanding areas like Katy or Richmond, it is best practice to calculate property taxes at around 2.5% to accurately reflect current market realities. This rate accounts for the base county taxes combined with Municipal Utility District (MUD) taxes, which fund new infrastructure.

- Insurance Premiums: Houston’s proximity to the Gulf Coast means higher insurance costs. Expect standard homeowners insurance to range from $2,000 to $5,000 annually. Additionally, if the property is in a designated flood zone within Harris County, separate flood insurance is mandatory.

- HOA Fees: Many master-planned communities have Homeowners Associations. Buyers often have to cover transfer fees, capitalization fees (often equal to one year of HOA dues), and the cost of the resale certificate ($100 – $500).

Seller Closing Costs in Houston

Sellers bear a different set of financial responsibilities at the closing table:

- Realtor Commissions: Usually the largest deduction from the seller’s proceeds, typically totaling 5% to 6% of the sale price, split between the listing agent and the buyer’s agent.

- Owner’s Title Insurance Policy: In Texas, it is customary (though entirely negotiable) for the seller to pay for the Owner’s Title Insurance, which protects the buyer’s equity in the home.

- Prorated Property Taxes: Because property taxes in Texas are paid in arrears (at the end of the year), the seller must credit the buyer for the portion of the year they owned the home.

2026 Houston Closing Costs by Price Point (Real Examples)

To give you a clearer picture, here is an estimated breakdown of buyer closing costs across different price tiers in the Houston area:

| Purchase Price | Estimated Buyer Closing Costs (2% – 5%) | Typical Houston Markets |

| $250,000 | $5,000 – $12,500 | Starter homes (Spring, Northeast Houston) |

| $350,000 | $7,000 – $17,500 | Median range (Pasadena, Pearland) |

| $450,000 | $9,000 – $22,500 | Move-up homes (Katy, Richmond, Cypress) |

| $600,000 | $12,000 – $30,000 | Premium (West University, Sugar Land) |

4 Ways Buyers Can Lower Closing Costs in Houston

- Negotiate Seller Concessions: If the market cools or a property has been sitting, you can ask the seller to contribute a percentage toward your closing costs.

- Shop for Mortgage Lenders: While title insurance rates are set by the state, lender fees are highly competitive. Compare Loan Estimates from at least three different lenders.

- Compare Home Insurance: Do not just take the first insurance quote. Shopping around for your homeowners and flood policies can significantly lower the initial amount required to fund your escrow account.

- Look for Down Payment Assistance: Programs through the Texas State Affordable Housing Corporation (TSAHC) or the City of Houston offer grants and favorable loan terms that can cover a substantial portion of your closing costs.

Frequently Asked Questions (FAQs)

Can I roll my closing costs into my mortgage in Texas? Typically, you cannot roll standard closing costs into a conventional loan. However, if you are using an FHA or VA loan, the upfront funding fees can be rolled into the loan balance. Alternatively, you can accept a slightly higher interest rate in exchange for “Lender Credits” to cover your out-of-pocket costs.

Who pays for title insurance in Houston? By long-standing local custom, the seller pays for the Owner’s Title Policy, while the buyer pays for the Lender’s Title Policy. Both are negotiable during the initial contract phase.

Are closing costs tax-deductible? Most closing costs, such as appraisal and origination fees, are not tax-deductible. However, the prepaid property taxes and mortgage discount points you pay at closing generally can be deducted on your federal tax return. Consult a CPA for specific advice.

Navigating the Texas real estate market requires more than just saving up for a down payment. By understanding exactly what goes into closing costs Houston, you can confidently budget for your property without any last-minute financial surprises at the title company.

Whether you are buying your first home or expanding your investment portfolio, having the right experts by your side makes all the difference. An experienced team will help you negotiate the best terms, find ways to lower your out-of-pocket expenses, and ensure a smooth path to the closing table.

Ready to make your move? Contact Win Nguyen Real Estate Group today to get a personalized estimate and turn your Texas real estate goals into reality!

Win Nguyen Group: Your Trusted Partner in Texas Real Estate.